Offering Details

Back

Under Review / Axiom Oil and Gas Inc.

Axiom Oil and Gas Inc.

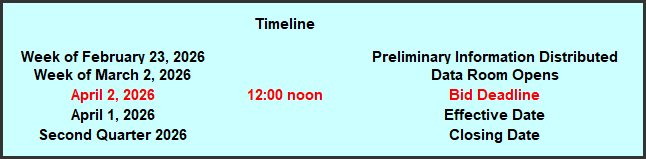

Bid Deadline: April 2, 2026

12:00 PM

Download Full PDF - Printable

OVERVIEW

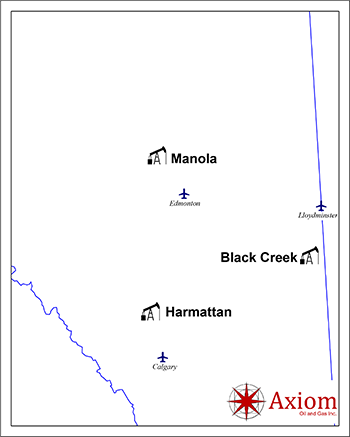

Axiom Oil and Gas Inc. (“Axiom” or the “Company”) has engaged Sayer Energy Advisors to assist it with the sale of certain of its oil and natural gas properties located in the Black Creek, Harmattan and Manola areas of Alberta (the “Properties”).

At Black Creek, Axiom holds an operated, 100% working interest. Production at Black Creek is primarily from the Cummings, Rex and Lloydminster of the Upper Mannville Group.

At Manola, Axiom holds various, primarily operated, working interests with an average 94% working interest. Production at Manola is primarily from the Basal Quartz Formation of the Lower Mannville Group.

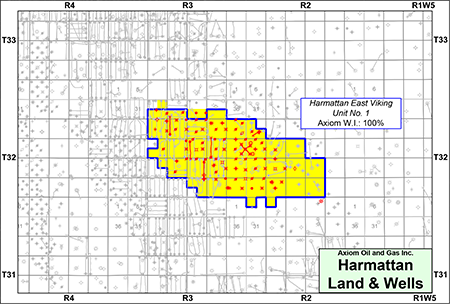

At Harmattan, Axiom holds various working interests including a 100% working interest in the Harmattan East Viking Unit No. 1.

Average daily sales production net to Axiom from the Properties for the year ended December 31, 2025 was approximately 786 boe/d, consisting of 545 barrels of oil and natural gas liquids per day and 1.5 MMcf/d of natural gas.

Actual operating income net to Axiom from the Properties for the year ended December 31, 2025 was approximately $6.8 million.

At Black Creek, Axiom holds an operated, 100% working interest. Production at Black Creek is primarily from the Cummings, Rex and Lloydminster of the Upper Mannville Group.

At Manola, Axiom holds various, primarily operated, working interests with an average 94% working interest. Production at Manola is primarily from the Basal Quartz Formation of the Lower Mannville Group.

At Harmattan, Axiom holds various working interests including a 100% working interest in the Harmattan East Viking Unit No. 1.

Average daily sales production net to Axiom from the Properties for the year ended December 31, 2025 was approximately 786 boe/d, consisting of 545 barrels of oil and natural gas liquids per day and 1.5 MMcf/d of natural gas.

Actual operating income net to Axiom from the Properties for the year ended December 31, 2025 was approximately $6.8 million.

Overview Map Showing the Location of the Divestiture Properties

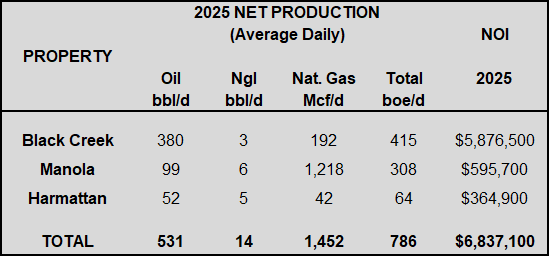

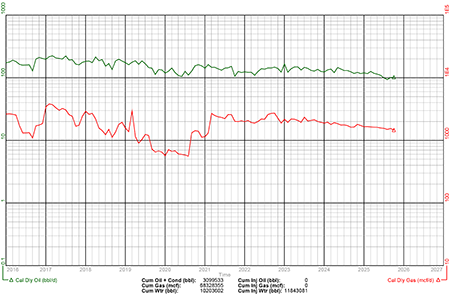

Production Overview

Average daily sales production net to Axiom from the Properties for the year ended December 31, 2025 was approximately 786 boe/d, consisting of 545 barrels of oil and natural gas liquids per day and 1.5 MMcf/d of natural gas.

Actual operating income net to Axiom from the Properties for the year ended December 31, 2025 was approximately $6.8 million.

Average daily sales production net to Axiom from the Properties for the year ended December 31, 2025 was approximately 786 boe/d, consisting of 545 barrels of oil and natural gas liquids per day and 1.5 MMcf/d of natural gas.

Actual operating income net to Axiom from the Properties for the year ended December 31, 2025 was approximately $6.8 million.

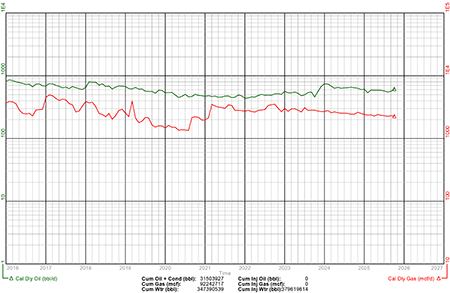

Gross Production Group Plot of the Properties

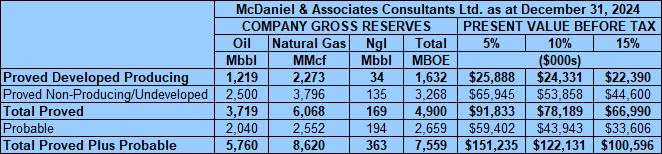

Reserves Overview

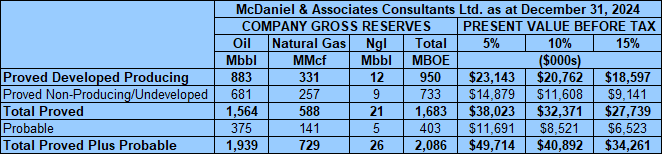

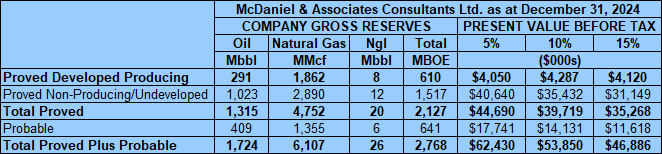

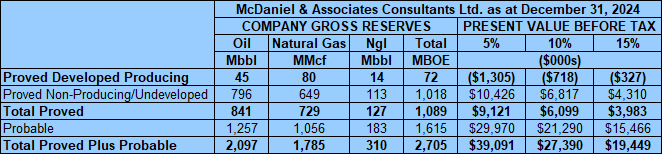

McDaniel & Associates Consultants Ltd. (“McDaniel”) prepared an independent reserves evaluation of the Properties as part of the Company’s year-end reporting (the “McDaniel Report”). The McDaniel Report is effective December 31, 2024 using an average of GLJ Ltd., McDaniel, and Sproule ERCE’s forecast pricing as at January 1, 2025.

McDaniel estimated that, as at December 31, 2024, the Properties contained remaining proved plus probable reserves of 6.1 million barrels of oil and natural gas liquids and 8.6 Bcf of natural gas (7.6 million boe), with an estimated net present value of $122.1 million using forecast pricing at a 10% discount.

McDaniel & Associates Consultants Ltd. (“McDaniel”) prepared an independent reserves evaluation of the Properties as part of the Company’s year-end reporting (the “McDaniel Report”). The McDaniel Report is effective December 31, 2024 using an average of GLJ Ltd., McDaniel, and Sproule ERCE’s forecast pricing as at January 1, 2025.

McDaniel estimated that, as at December 31, 2024, the Properties contained remaining proved plus probable reserves of 6.1 million barrels of oil and natural gas liquids and 8.6 Bcf of natural gas (7.6 million boe), with an estimated net present value of $122.1 million using forecast pricing at a 10% discount.

Marketing Summary

Axiom has marketing contracts in place with Shell Trading Canada for oil and Suncor Energy Inc. for natural gas and liquids.

Further details of the marketing arrangements will be made available in the virtual data room for parties that execute a confidentiality agreement.

Liablity Assessment

As of January 1, 2026, the Properties had a deemed liability value of $28.9 million.

Axiom has marketing contracts in place with Shell Trading Canada for oil and Suncor Energy Inc. for natural gas and liquids.

Further details of the marketing arrangements will be made available in the virtual data room for parties that execute a confidentiality agreement.

Liablity Assessment

As of January 1, 2026, the Properties had a deemed liability value of $28.9 million.

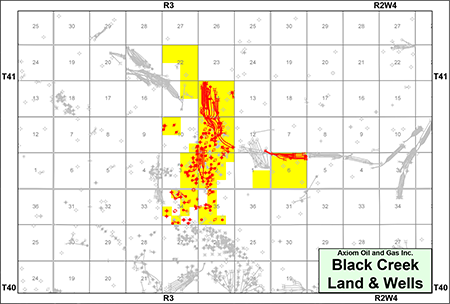

BLACK CREEK

Township 40-41, Range 2-3 W4

At Black Creek, Axiom holds an operated, 100% working interest. Production at Black Creek is primarily from the Cummings, Rex and Lloydminster of the Upper Mannville Group.

Average daily sales production net to Axiom from Black Creek for the year ended December 31, 2025 was approximately 415 boe/d, consisting of 383 barrels of oil and natural gas liquids per day and 192 Mcf/d of natural gas.

Operating income net to Axiom from Black Creek for the year ended December 31, 2025 was approximately $5.9 million.

Oil production at Black Creek is currently limited by injection capacity. The Company believes oil production can be immediately increased by repairing a pipeline, reactivating wells and chemically stimulating the injectors. Axiom has identified further near-term oil potential by performing certain reactivations and increasing pump speed on existing vertical wells.

At Black Creek, Axiom holds an operated, 100% working interest. Production at Black Creek is primarily from the Cummings, Rex and Lloydminster of the Upper Mannville Group.

Average daily sales production net to Axiom from Black Creek for the year ended December 31, 2025 was approximately 415 boe/d, consisting of 383 barrels of oil and natural gas liquids per day and 192 Mcf/d of natural gas.

Operating income net to Axiom from Black Creek for the year ended December 31, 2025 was approximately $5.9 million.

Oil production at Black Creek is currently limited by injection capacity. The Company believes oil production can be immediately increased by repairing a pipeline, reactivating wells and chemically stimulating the injectors. Axiom has identified further near-term oil potential by performing certain reactivations and increasing pump speed on existing vertical wells.

Black Creek, Alberta

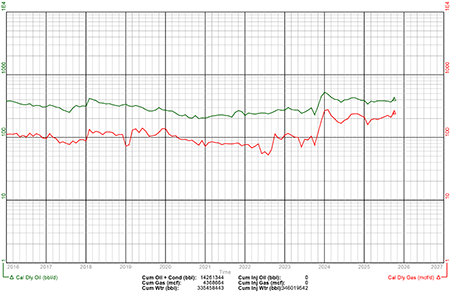

Gross Production Group Plot of Axiom's Oil & Natural Gas Wells

Black Creek Upside

The target formations at Black Creek consist of the Rex, Cummings and Lloydminster formations of the Mannville Group. The Rex is made up of transgressive and regressive deposits of thin sands and shales separated by lithic channels. The Lloydminster is made up of shoreline deposits with abundant coal and sand. The Dina/Cummings are marine and non-marine deposits of sandstone and interbedded siltstones overlain by a thick coal package.

The target formations at Black Creek consist of the Rex, Cummings and Lloydminster formations of the Mannville Group. The Rex is made up of transgressive and regressive deposits of thin sands and shales separated by lithic channels. The Lloydminster is made up of shoreline deposits with abundant coal and sand. The Dina/Cummings are marine and non-marine deposits of sandstone and interbedded siltstones overlain by a thick coal package.

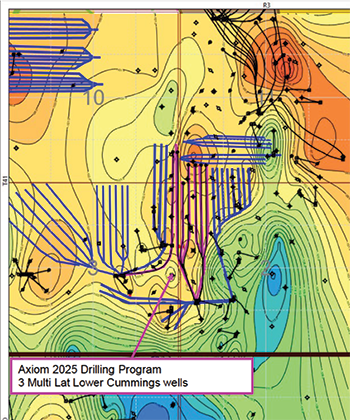

Axiom drilled two multi-lateral wells, Axiom Provost 05/01-10-041-03W4/0 and Axiom Hz 06 Provost 06/04-11-041-03W4/0 on its lands at Black Creek in 2025 with initial production rates of approximately 84 bbl/d and 94 bbl/d of oil.

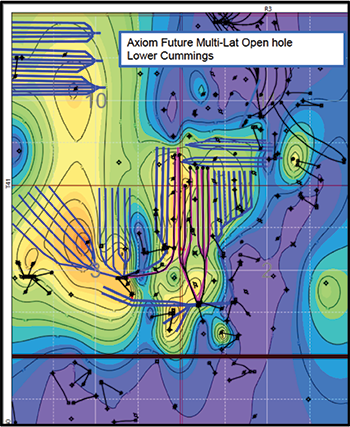

Through this drilling, the Company believes it has derisked 14 additional multilateral wells. The Company has also identified a recompletion opportunity at 02/01-10-041-03W4.

Through this drilling, the Company believes it has derisked 14 additional multilateral wells. The Company has also identified a recompletion opportunity at 02/01-10-041-03W4.

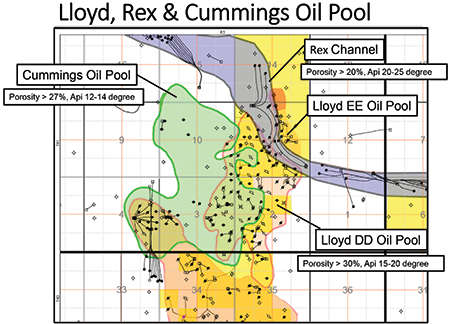

The Cummings oil pool has porosity of approximately 21%, with average net pay of 2 m thick, clean sand. The water saturation is 25%, current cumulative oil production is approximately 113 Mbbl with oil in place of about 3.9 MMbbl. The total area is 509 acres and recovery factor to date is 2.9% of 20° API oil.

AOAGI Axiom Provost 100/09-03-041-03W4/0

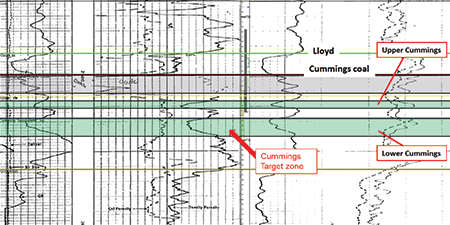

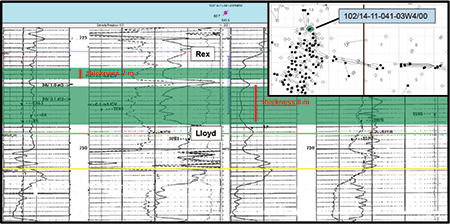

Cummings Formation Type Log

Cummings Formation Type Log

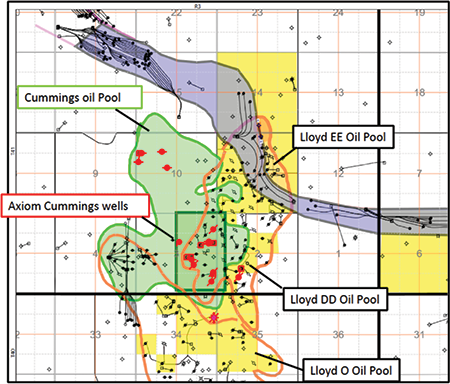

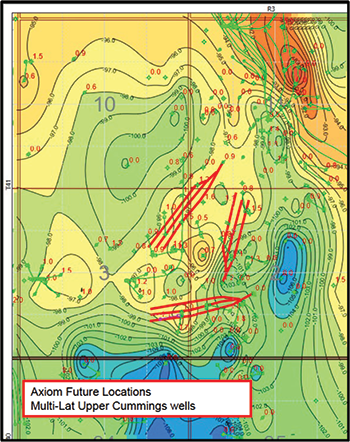

The Cummings pool is outlined in green in the following map.

Lower Cummings Structure and Net Pay Maps

Upper Cummings Structure and Net Pay Maps

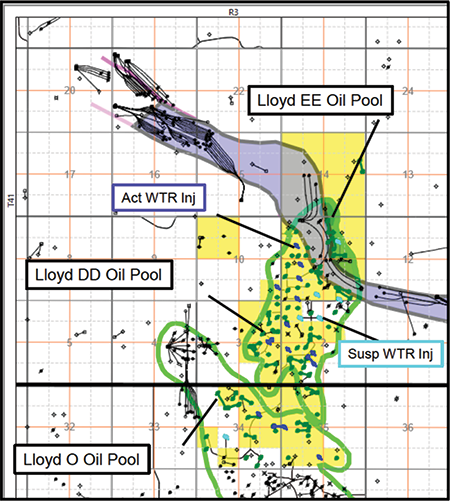

The Lloydminster is made up of separate oil pools separated by a deeply incised Rex channel with a structural low to the south. In the DD and EE pools, average net pay is approximately 4 m, porosity is 27-30%, with permeability of 0.5-1 D and water saturation of 65-80%. Current cumulative oil production is approximately 113 Mbbl with oil in place of about 3.9 MMbbl. The total area is 972 acres and recovery factor to date is 52% of 15-20° API oil.

There have been no horizontal wells drilled in the Lloydminster Formation to date at Black Creek.

There have been no horizontal wells drilled in the Lloydminster Formation to date at Black Creek.

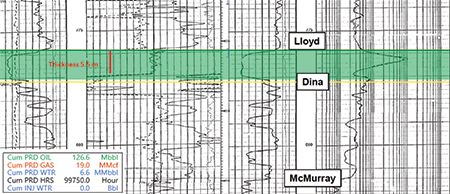

AOAGI Axiom Provost 105/09-03-041-03W4/0

Lloydminster Formation Type Log

Renaissance 14D Provost 102/14-11-041-03W4/0

Lloydminster Formation Type Log

Lloydminster Formation Type Log

Renaissance 14D Provost 102/14-11-041-03W4/0

Lloydminster Formation Type Log

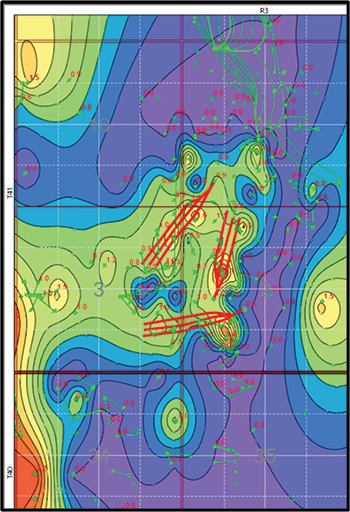

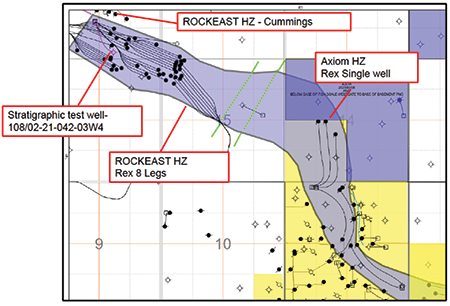

The Rex channel at Black Creek is shown on the following map.

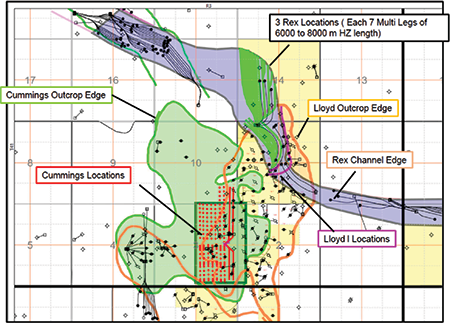

The Company has identified 4 horizontal wells with 6 lateral legs, each with 6,000-8,000 m of length.

Further technical information will be made available in the virtual data room for parties that execute a confidentiality agreement.

Black Creek Facilities

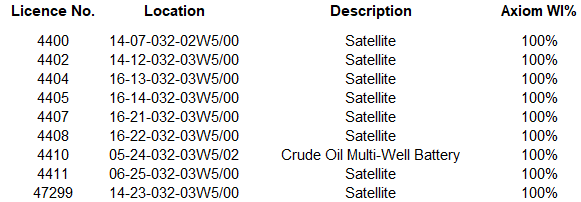

The Company holds working interests in the following facilities at Black Creek.

Further technical information will be made available in the virtual data room for parties that execute a confidentiality agreement.

Black Creek Facilities

The Company holds working interests in the following facilities at Black Creek.

Black Creek Reserves

McDaniel & Associates Consultants Ltd. (“McDaniel”) prepared an independent reserves evaluation of the Properties as part of the Company’s year-end reporting (the “McDaniel Report”). The McDaniel Report is effective December 31, 2024 using an average of GLJ Ltd., McDaniel, and Sproule ERCE’s forecast pricing as at January 1, 2025.

McDaniel estimated that, as at December 31, 2024, the Black Creek property contained remaining proved plus probable reserves of 2.0 million barrels of oil and natural gas liquids and 729 MMcf of natural gas (2.1 million boe), with an estimated net present value of $40.9 million using forecast pricing at a 10% discount.

McDaniel & Associates Consultants Ltd. (“McDaniel”) prepared an independent reserves evaluation of the Properties as part of the Company’s year-end reporting (the “McDaniel Report”). The McDaniel Report is effective December 31, 2024 using an average of GLJ Ltd., McDaniel, and Sproule ERCE’s forecast pricing as at January 1, 2025.

McDaniel estimated that, as at December 31, 2024, the Black Creek property contained remaining proved plus probable reserves of 2.0 million barrels of oil and natural gas liquids and 729 MMcf of natural gas (2.1 million boe), with an estimated net present value of $40.9 million using forecast pricing at a 10% discount.

Black Creek Liability Assessment

As of January 1, 2026, the Black Creek property had a deemed liability value of $7.1 million.

Black Creek Well List

Click here to download the complete well list in Excel.

As of January 1, 2026, the Black Creek property had a deemed liability value of $7.1 million.

Black Creek Well List

Click here to download the complete well list in Excel.

MANOLA

Township 57-61, Range 1-7 W5

At Manola, Axiom holds various, primarily operated working interests. Production at Manola is primarily from the Basal Quartz Formation of the Lower Mannville Group.

Average daily sales production net to Axiom from Manola for the year ended December 31, 2025 was approximately 308 boe/d, consisting of 1.2 MMcf/d of natural gas and 105 barrels of oil and natural gas liquids per day.

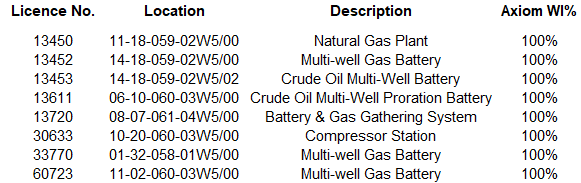

At Manola, Axiom has 100% working interests in natural gas processing plant located at 11-18-059-02W5/00.

Operating income net to Axiom from Manola for the year ended December 31, 2025 was approximately $596,000.

At Manola, Axiom holds various, primarily operated working interests. Production at Manola is primarily from the Basal Quartz Formation of the Lower Mannville Group.

Average daily sales production net to Axiom from Manola for the year ended December 31, 2025 was approximately 308 boe/d, consisting of 1.2 MMcf/d of natural gas and 105 barrels of oil and natural gas liquids per day.

At Manola, Axiom has 100% working interests in natural gas processing plant located at 11-18-059-02W5/00.

Operating income net to Axiom from Manola for the year ended December 31, 2025 was approximately $596,000.

Manola, Alberta

Gross Production Group Plot of Axiom's Oil & Natural Gas Wells

Manola Upside

The Company had a reservoir study done by Weatherford Petroleum Consultants AS which supports development through future horizontal drilling at Manola. The Weatherford report will be available in the virtual data room for parties that execute a confidentiality agreement.

Axiom estimates that oil recovery from Manola to date is approximately 7% of oil in place mainly from existing legacy vertical wells. Horizontal drilling is required to enhance recoveries, as supported by the Weatherford study.

The Company has also identified approximately 130 boe/d (50 bbl/d of oil and 500 Mcf/d of solution natural gas) of production which is currently offline from 20 wells with holes in tubing requiring repair.

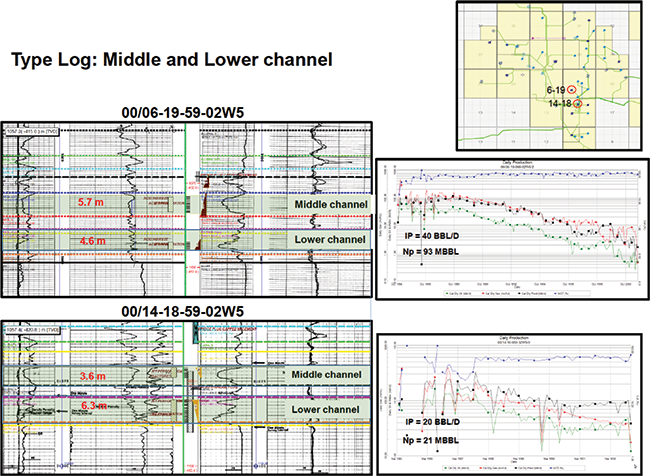

The Basal Quartz Formation at Manola was deposited during the early Cretaceous. The Formation is interpreted as fluvial-deltaic environment and contains a sequence of interbedded sandstone, siltstone and shale.

The different reservoirs are identified as channels systems.

The Company had a reservoir study done by Weatherford Petroleum Consultants AS which supports development through future horizontal drilling at Manola. The Weatherford report will be available in the virtual data room for parties that execute a confidentiality agreement.

Axiom estimates that oil recovery from Manola to date is approximately 7% of oil in place mainly from existing legacy vertical wells. Horizontal drilling is required to enhance recoveries, as supported by the Weatherford study.

The Company has also identified approximately 130 boe/d (50 bbl/d of oil and 500 Mcf/d of solution natural gas) of production which is currently offline from 20 wells with holes in tubing requiring repair.

The Basal Quartz Formation at Manola was deposited during the early Cretaceous. The Formation is interpreted as fluvial-deltaic environment and contains a sequence of interbedded sandstone, siltstone and shale.

The different reservoirs are identified as channels systems.

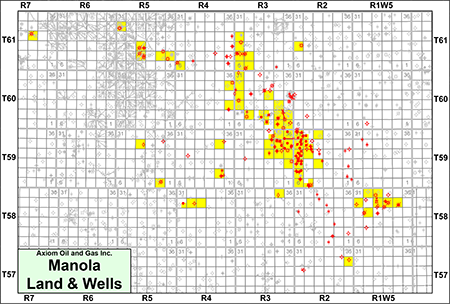

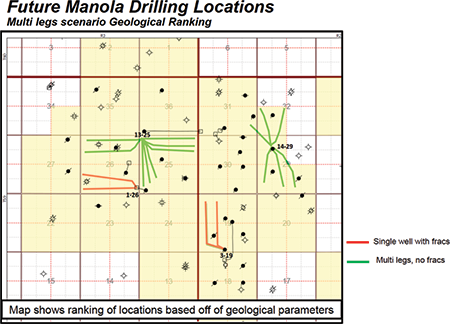

Axiom has identified low-cost upside in low-risk single and multi-leg drilling locations. The well pads for these locations would be located at 03-19-059-02W5, 13-25-059-03W5, 01-26-059-03W5 and 14-29-059-03W5.

The Company’s drilling locations and recompletion opportunities at Manola are shown on the following map.

The Company’s drilling locations and recompletion opportunities at Manola are shown on the following map.

Further technical information will be made available in the virtual data room for parties that execute a confidentiality agreement.

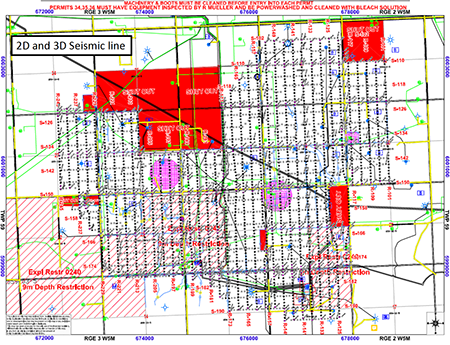

Manola Seismic

The Company has trade 2D and 3D seismic data over a portion of its lands at Manola. Information relating to the seismic will be made available in the virtual data room to parties that execute a confidentiality agreement.

Manola Seismic

The Company has trade 2D and 3D seismic data over a portion of its lands at Manola. Information relating to the seismic will be made available in the virtual data room to parties that execute a confidentiality agreement.

Manola Facilities

The Company holds working interests in the following facilities at Manola.

The Company holds working interests in the following facilities at Manola.

Manola Reserves

McDaniel & Associates Consultants Ltd. (“McDaniel”) prepared an independent reserves evaluation of the Properties as part of the Company’s year-end reporting (the “McDaniel Report”). The McDaniel Report is effective December 31, 2024 using an average of GLJ Ltd., McDaniel, and Sproule ERCE’s forecast pricing as at January 1, 2025.

McDaniel estimated that, as at December 31, 2024, the Manola property contained remaining proved plus probable reserves of 6.1 Bcf of natural gas and 1.8 million barrels of oil and natural gas liquids (2.8 million boe), with an estimated net present value of $53.9 million using forecast pricing at a 10% discount.

McDaniel & Associates Consultants Ltd. (“McDaniel”) prepared an independent reserves evaluation of the Properties as part of the Company’s year-end reporting (the “McDaniel Report”). The McDaniel Report is effective December 31, 2024 using an average of GLJ Ltd., McDaniel, and Sproule ERCE’s forecast pricing as at January 1, 2025.

McDaniel estimated that, as at December 31, 2024, the Manola property contained remaining proved plus probable reserves of 6.1 Bcf of natural gas and 1.8 million barrels of oil and natural gas liquids (2.8 million boe), with an estimated net present value of $53.9 million using forecast pricing at a 10% discount.

Manola Liability Assessment

As of January 1, 2026, the Manola property had a deemed liability value of $11.6 million.

Manola Well List

Click here to download the complete well list in Excel.

As of January 1, 2026, the Manola property had a deemed liability value of $11.6 million.

Manola Well List

Click here to download the complete well list in Excel.

HARMATTAN

Township 32-33, Range 2-3 W5

At Harmattan, Axiom holds various working interests including a 100% working interest in the Harmattan East Viking Unit No. 1.

Oil and natural gas production from the Viking Formation at Harmattan is produced to a multi-well battery located at 05-24-032-03W5. The property was developed originally with vertical wells and has only four horizontal wells drilled to date located at 06-15-032-03W5, 13-22-032-03W5, 04-23-032-03W5, and 04-28-032-03W5. The property also has water injection wells in place.

Average daily sales production net to Axiom from Harmattan for the year ended December 31, 2025 was approximately 64 boe/d, consisting of 57 barrels of oil and natural gas liquids per day and 42 Mcf/d of natural gas.

Operating income net to Axiom from Harmattan for the year ended December 31, 2025 was approximately $365,000.

At Harmattan, Axiom holds various working interests including a 100% working interest in the Harmattan East Viking Unit No. 1.

Oil and natural gas production from the Viking Formation at Harmattan is produced to a multi-well battery located at 05-24-032-03W5. The property was developed originally with vertical wells and has only four horizontal wells drilled to date located at 06-15-032-03W5, 13-22-032-03W5, 04-23-032-03W5, and 04-28-032-03W5. The property also has water injection wells in place.

Average daily sales production net to Axiom from Harmattan for the year ended December 31, 2025 was approximately 64 boe/d, consisting of 57 barrels of oil and natural gas liquids per day and 42 Mcf/d of natural gas.

Operating income net to Axiom from Harmattan for the year ended December 31, 2025 was approximately $365,000.

Harmattan, Alberta

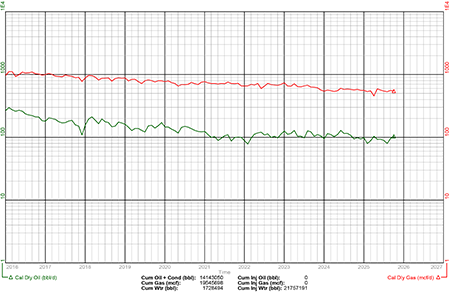

Gross Production Group Plot of Axiom's Oil & Natural Gas Wells

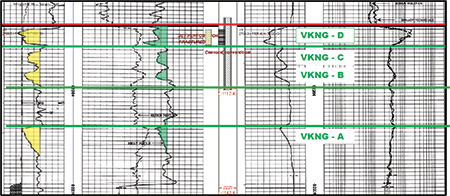

Viking Formation

The Early Cretaceous Viking Formation is a member of the Colorado Group which overlies the marine shales of the Joli Fou Formation and is overlain by the Lower Colorado Shale. Deposition is thought to have been in a shallow marine environment and has been interpreted as comprising four cycles of regressive clastic wedges of coarsening upward shelf to shoreface parasequence.

The sequence boundary truncates by a superimposed ravinement surface of high shaly beds. Each sequence is identified on the following logs as Viking A to D where Viking A is the oldest and thickest one in the section. Viking D is chert pebble conglomerate, high porosity, but very abrasive on drill bits and it is the primary producing zone in the area.

According to fracture modeling, the Company recognizes that fracture treatments targeting the Viking D largely grow downward resulting in very low proppant concentration in target Viking D zone.

There is some production coming from Viking C sandstone with high porosity, low permeability.

Axiom plans to recomplete some wells in the thick Viking A to evaluate this resource.

The Harmattan Viking oil pool is about 8-12% porosity with average net pay of 4-6 m of thick, clean sand. The reservoir has permeability between 10 to 200 mD, water saturation of 35%, initial reservoir pressure of approximately 16,000 Kpa and current reservoir pressure around 1,200 – 5,000 Kpa. Current cumulative production is approximately 13 MMbbl and oil in place is about 120 MMbbl with the total area calculated at 13,458 acres and a recovery factor to date of 11%.

The Early Cretaceous Viking Formation is a member of the Colorado Group which overlies the marine shales of the Joli Fou Formation and is overlain by the Lower Colorado Shale. Deposition is thought to have been in a shallow marine environment and has been interpreted as comprising four cycles of regressive clastic wedges of coarsening upward shelf to shoreface parasequence.

The sequence boundary truncates by a superimposed ravinement surface of high shaly beds. Each sequence is identified on the following logs as Viking A to D where Viking A is the oldest and thickest one in the section. Viking D is chert pebble conglomerate, high porosity, but very abrasive on drill bits and it is the primary producing zone in the area.

According to fracture modeling, the Company recognizes that fracture treatments targeting the Viking D largely grow downward resulting in very low proppant concentration in target Viking D zone.

There is some production coming from Viking C sandstone with high porosity, low permeability.

Axiom plans to recomplete some wells in the thick Viking A to evaluate this resource.

The Harmattan Viking oil pool is about 8-12% porosity with average net pay of 4-6 m of thick, clean sand. The reservoir has permeability between 10 to 200 mD, water saturation of 35%, initial reservoir pressure of approximately 16,000 Kpa and current reservoir pressure around 1,200 – 5,000 Kpa. Current cumulative production is approximately 13 MMbbl and oil in place is about 120 MMbbl with the total area calculated at 13,458 acres and a recovery factor to date of 11%.

Axiom Harme 100/16-13-032-03W5

Viking Formation Type Log

Viking Formation Type Log

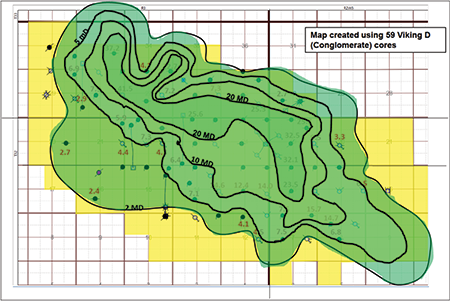

The following image shows the average permeability within the Viking reservoir at Harmattan.

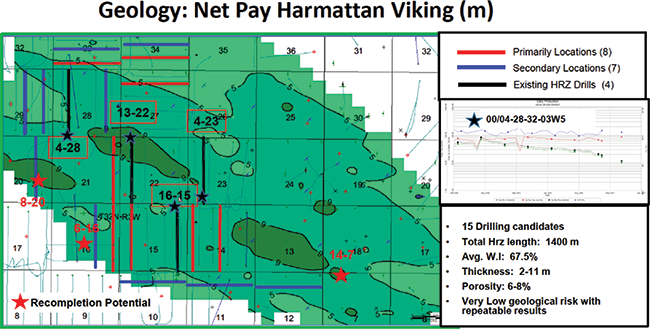

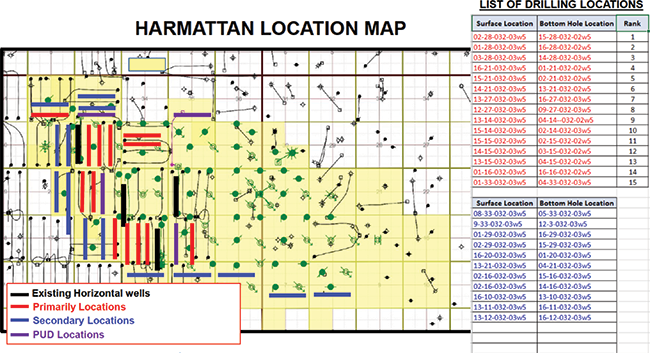

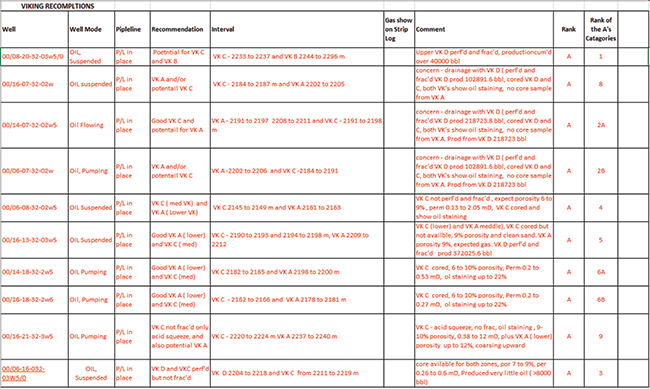

The Company’s drilling locations and recompletion opportunities at Harmattan are shown on the following net pay map along with the four existing horizontal wells within the Unit.

Additional drilling locations are listed below and are also shown on the following map.

The Viking recompletions are outlined in the table below.

Further technical information will be made available in the virtual data room for parties that execute a confidentiality agreement.

Harmattan Facilities

The Company holds working interests in the following facilities at Harmattan.

Harmattan Facilities

The Company holds working interests in the following facilities at Harmattan.

Harmattan Reserves

McDaniel & Associates Consultants Ltd. (“McDaniel”) prepared an independent reserves evaluation of the Properties as part of the Company’s year-end reporting (the “McDaniel Report”). The McDaniel Report is effective December 31, 2024 using an average of GLJ Ltd., McDaniel, and Sproule ERCE’s forecast pricing as at January 1, 2025.

McDaniel estimated that, as at December 31, 2024, the Harmattan property contained remaining proved plus probable reserves of 2.4 million barrels of oil and natural gas liquids and 1.8 Bcf of natural gas (2.7 million boe), with an estimated net present value of $27.4 million using forecast pricing at a 10% discount.

McDaniel & Associates Consultants Ltd. (“McDaniel”) prepared an independent reserves evaluation of the Properties as part of the Company’s year-end reporting (the “McDaniel Report”). The McDaniel Report is effective December 31, 2024 using an average of GLJ Ltd., McDaniel, and Sproule ERCE’s forecast pricing as at January 1, 2025.

McDaniel estimated that, as at December 31, 2024, the Harmattan property contained remaining proved plus probable reserves of 2.4 million barrels of oil and natural gas liquids and 1.8 Bcf of natural gas (2.7 million boe), with an estimated net present value of $27.4 million using forecast pricing at a 10% discount.

Harmattan Liability Assessment

As of January 1, 2026, the Harmattan property had a deemed liability value of $10.4 million.

Harmattan Well List

Click here to download the complete well list in Excel.

As of January 1, 2026, the Harmattan property had a deemed liability value of $10.4 million.

Harmattan Well List

Click here to download the complete well list in Excel.

PROCESS & TIMELINE

Sayer Energy Advisors is accepting cash offers to acquire the Properties until 12:00 pm on Thursday April 2, 2026.

Sayer Energy Advisors does not typically conduct a "second-round" bidding process; the intention is to attempt to conclude

transactions with the parties submitting the most acceptable proposals at the conclusion of the process.

transactions with the parties submitting the most acceptable proposals at the conclusion of the process.

Sayer Energy Advisors is accepting cash offers from interested parties until

noon on Thursday April 2, 2026.

NOTE REGARDING A SAYER PROCESS

On each and every offering brochure generated by Sayer, you will note the sentence “Sayer Energy Advisors does not conduct a “second-round” bidding process; the intention is to attempt to conclude a sale of the Properties with the party submitting the most acceptable proposal at the conclusion of the process.” What this means is that Sayer will not go back to multiple parties at the same time after bids are received, asking them all for a second bid. We determine which party submitted the most acceptable proposal and then we attempt to negotiate acceptable terms with that party in a “one-off” situation.

If the process involves a cash sale of a property or company and the party which submitted the most acceptable proposal has met our client’s threshold value, that offer will be accepted. If this proposal does not meet our client’s threshold value, then we will advise that party that the offer is not quite what our client was expecting, and we will ask them to increase the offer. If that offer is not acceptable to our client, we will then move down to the party which submitted the next most acceptable proposal and we will then work with that party to attempt to meet our client’s threshold value.

In the extremely rare circumstance where two or more parties submit virtually identical proposals, we will contact all parties, we will advise them of this situation and we will ask them to submit a revised proposal. Once these are received, we will work with the party which has submitted the most acceptable proposal.If the process involves a cash sale of a property or company and the party which submitted the most acceptable proposal has met our client’s threshold value, that offer will be accepted. If this proposal does not meet our client’s threshold value, then we will advise that party that the offer is not quite what our client was expecting, and we will ask them to increase the offer. If that offer is not acceptable to our client, we will then move down to the party which submitted the next most acceptable proposal and we will then work with that party to attempt to meet our client’s threshold value.

CONFIDENTIALITY AGREEMENT

Parties wishing to receive access to the confidential information with detailed technical information relating to this opportunity should execute the Confidentiality Agreement and return one copy to Sayer Energy Advisors by courier, email (tpavic@sayeradvisors.com) or fax (403.266.4467).

Included in the confidential information is the following: summary land information, the McDaniel Report, deemed liability information, most recent net operations summary, detailed facilities information and other relevant technical information.

Download Confidentiality Agreement

To receive further information on the Properties please contact Tom Pavic, Ben Rye or Sydney Birkett at 403.266.6133.